Message from the CFO

Accelerating business growth and the increase of corporate value from six key perspectives

Review of FY2025

In FY2025, EPS increased significantly by 110 yen year on year to 182 yen, nearly reaching the target level, while ROIC was 7.6%, exceeding the target of 7.2%. This performance was driven by strong results across our operating companies, with all segments—Alcoholic Beverages, Non-alcoholic Beverages, Pharmaceuticals, and Health Science—achieving their normalized operating profit targets. In particular, the Health Science Business recorded a profit of 11.1 billion yen. This was supported by the successful closing on July 1 of the divestiture of Kyowa Hakko Bio’s amino acid business and other businesses, which had originally been expected to take until the end of 2025, as well as by the continued growth of Blackmores and FANCL in line with our expectations following their M&As. These outcomes reflect an improvement in our execution. Based on the current stock price, we believe that investors are recognizing our management efforts to a certain extent.

The role of the CFO is to advance management strategy from both financial and non-financial perspectives. In line with the direction set out in KV2027, we believe we have established a business portfolio that enables sustainable growth across the Group. We also believe that the enhanced “earning power” of each segment and the achievement of our normalized operating profit targets represent a significant accomplishment.

New Long-Term Vision

Seven years have passed since the launch of KV2027. During this time, we have steadily advanced the transformation toward our target business portfolio while establishing a framework for global Group management. We have also responded flexibly to changes in the external environment that were not anticipated at the time KV2027 was formulated, including heightened geopolitical risks and the COVID-19 pandemic.

As we approach 2027 next year, we have launched our new Long- Term Vision, “Innovate2035!”, starting this year with a view to the next decade. There are no significant changes from the direction we have pursued under KV2027. Now that we have established our business portfolio, clarified the roles of each business, and developed our management framework, we are entering a new stage in which each business will grow autonomously. In particular, we aim to steadily advance the global standardization of our management systems. To this end, the following “changes” will be implemented.

-

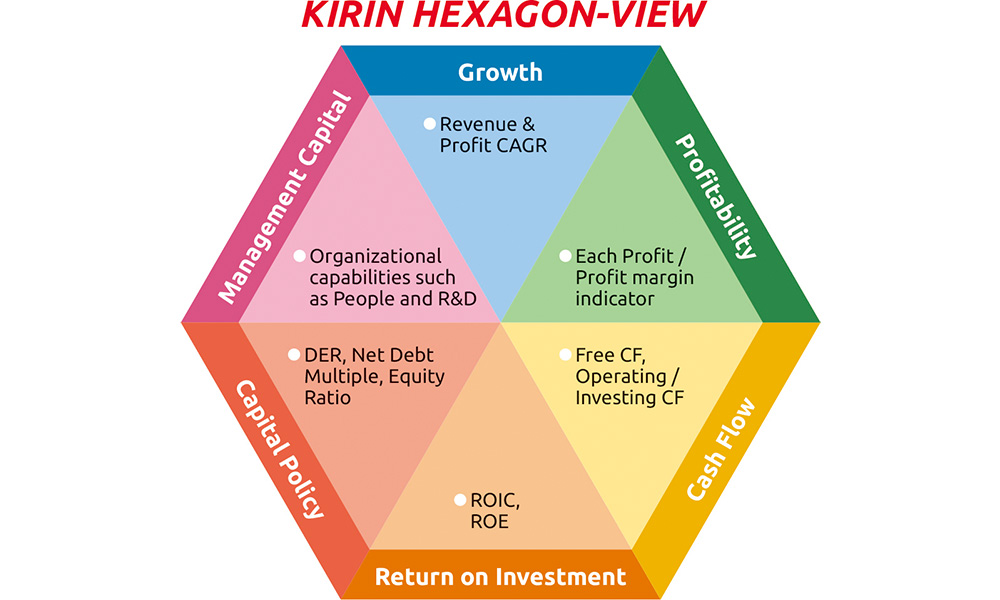

To ensure that strategic dialogue between corporate and operating companies is not overly focused on normalized operating profit, we will manage the business in a balanced manner across six key perspectives (KIRIN HEXAGON-VIEW).

-

For domestic operating companies, as a certain level of efficiency has been achieved through the integration of indirect functions, we will transfer selected frontline functions to these companies so that they can autonomously improve and streamline their operations.

-

While management systems have differed across operating companies to date, we will progressively transition to a globally standardized management system utilizing SAP.

Six key perspectives – KIRIN HEXAGON-VIEW

Currently, across the Kirin Group, each operating company conducts financial modeling looking ahead 10 years. Based on this, corporate and the operating companies engage in dialogue on identifying growth drivers, related investments, and risk factors. These financial models are reviewed annually to reflect performance results and environmental changes. Based on a rolling three-year outlook, we disclose three-year targets to investors.

This rolling three-year approach was formally introduced last year, replacing the fixed three-year medium-term plan, although it had already been implemented at the operational level several years earlier. From FY2026, we will place greater emphasis on adapting agilely to current environmental changes while moving toward our new Long-Term Vision, as well as on allocating more resources to execution rather than to planning itself.

We will continue to engage in dialogue with operating companies based on rolling plans grounded in financial modeling. The perspectives applied in this process have been newly organized as the KIRIN HEXAGON-VIEW. As you will see, it does not present anything particularly new. However, we believe that its value lies in establishing a common language across the Group. Given the differences among businesses—such as Alcoholic Beverages, Health Science and Non-alcoholic Beverages, and Pharmaceuticals—as well as regional differences across Japan, APAC, and North America, it is becoming increasingly important to apply clear criteria and strengthen alignment of the finance function throughout businesses.

In terms of perspective, operating companies have tended to focus excessively on short-term normalized operating profit and adopt a P&L-oriented approach. However, now that structural reforms aimed at transforming our business portfolio and establishing a solid earnings base have largely been completed, we will place greater emphasis than ever on a forward-looking perspective with a balance sheet- and cash flow-oriented approach. From the corporate CFO function, we will engage in dialogue with each business while taking a holistic, Group-wide perspective and allocate cash in a manner that enables EPS growth and ROIC improvement over the long, medium, and short term. In other words, when structural reforms are required in a particular business from a long-term perspective—even if they have a negative impact on short-term bottom-line profit—we will restrain lower-priority investments in other businesses. By doing so, we aim to achieve the Group’s short-term targets while ensuring that we do not undermine the foundations for sustainable growth in individual businesses.

In addition, we have established regional financial management companies in APAC, China, and North America, and have begun operations under which these entities manage funding and investment within each region, while also overseeing cash control across the Group. Some of these regional financial management companies are expected to take on tax management functions in the future, further enhancing our global tax governance. These initiatives are also aimed at continuously strengthening the Group’s cash generation capabilities.

KIRIN HEXAGON-VIEW was shared across the Group at the Global CFO Meeting held in September 2025, which brought together the heads of finance functions from major operating companies in Japan and overseas. We develop financial models looking ahead 10 years and, based on these, refine our rolling three-year outlook with greater precision. To maximize these benefits, we will engage in transparent dialogue with operating companies based on consistent perspectives, and steadily increase corporate value across the Group.

Transfer of frontline functions

Under our new Long-Term Vision, we aim to achieve both “autonomous growth of each business domain and operating company” and “growth via cross-domain collaboration.” To realize this, we have reviewed and clarified the functions that should be undertaken by corporate and those that should be held by operating companies.

The Kirin Group introduced a pure holding company structure in 2007 and rapidly expanded its overseas operations. During a period when we actively pursued overseas acquisitions, we adopted a federal-style management structure with regional headquarters in each region. In Japan as well, a regional headquarters was established to consolidate indirect functions across domestic operating companies. However, following the subsequent merger of the Japan headquarters with Kirin Holdings, certain frontline functions still remain within Kirin Holdings today.

Now that the direction of each business has been clearly defined, we will return these frontline functions to the operating companies. This will support autonomous profit growth while enabling each business to streamline and reduce lower-priority activities based on its own judgment. The transfer of these frontline functions is expected to be completed within one to two years. The standardization of monitoring perspectives through KIRIN HEXAGON-VIEW—particularly the shift away from an excessive focus on normalized operating profit—is an essential foundation for this transition.

Standardization and quantification of management data

We have introduced SAP as our ERP system across many operating companies. Like many Japanese companies, our Group previously relied on internally developed proprietary systems. However, taking into account the organizational capabilities of our IT function and security considerations, we have been progressing the transition to SAP. In this regard, the migration to SAP can be considered to have proceeded smoothly. On the other hand, despite the fact that many operating companies are using the same SAP system, the way data is structured and defined has not been standardized, and it cannot yet be said that we are fully utilizing it as a management system. Looking at the external environment, AI is advancing rapidly. By urgently standardizing data structures and definitions and becoming a leader in AI utilization, we can establish a competitive advantage.

First, in our dialogue with operating companies as described above, we aim to ensure that both corporate and operating companies consistently work from the same data, so as to avoid any misalignment. By implementing SAP at Blackmores and FANCL and thoroughly applying a Fit-to-Standard approach, we aim to achieve integrated operations in the Health Science Business by FY2028.

We will then leverage these learnings across other business domains, including the Alcoholic Beverages Business, and aim to establish the foundation for unified infrastructure as early as FY2030.

Next is risk-taking. To support operating companies in taking risks for growth, we are advancing the quantification of risk. At Kirin Holdings, there are teams within both the corporate strategy function and the finance function that oversee risk management from their respective functional perspectives. In addition, the finance function has launched initiatives to quantify risk, incorporating FP&A and treasury capabilities. Following trial initiatives at both domestic and overseas operating companies, we plan to establish a model by FY2028 and roll it out across the Group. While avoiding risks that should be avoided, we will clearly define the level of risk the Group can take based on its financial strength, and proactively take risks where returns can be quantitatively expected to exceed those risks, thereby contributing to the increase of corporate value.

Finally, we turn to investment in non-financial capital. In our Long-Term Vision, we refer R&D, marketing, and AI as “organizational capabilities to continuously create innovation,” positioning them and the human capital that drives execution as key non-financial capital.

As noted in the previous Integrated Report, we have established the Corporate Disclosure Section within the Finance Department. The Corporate Disclosure Section is an organization within the finance function aimed at making non-financial capital visible in corporate value. In FY2025, it worked to achieve the early implementation of SSBJ-aligned disclosures and to enhance the visibility of how non-financial factors are linked to financial outcomes.

With regard to the former, in our Annual Securities Report issued on March 27, 2026, we became the first Japanese company to provide disclosures in accordance with the SSBJ standards. We disclosed material sustainability-related risks and opportunities, as well as their financial impacts, in a manner that enhances international comparability. As a “global leader in CSV,” we made these disclosures three years ahead of the mandatory requirement. However, our objective is not disclosure itself. By disclosing early, we aim to accelerate the accumulation and integration of non-financial data and transition to data utilization as quickly as possible.

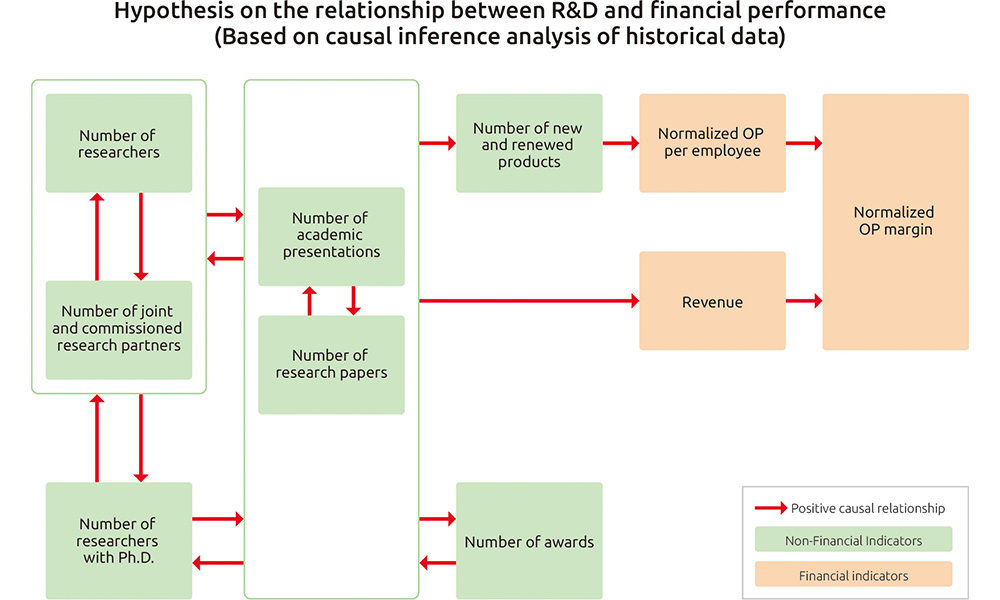

Causal analysis of the relationship between non-financial and financial factors is also not undertaken for the purpose of disclosure itself. Rather, it is intended to support investment decisions based on hypotheses as to whether investments in human capital, R&D, marketing, and AI will lead to an increase corporate value in the future. Through a joint project with Fujitsu Limited, we analyzed historical data on both non-financial and financial performance in human capital and intellectual capital (R&D and AI) using causal inference. This analysis has provided insights into which non-financial indicators, when improved, may have a positive financial impact, as well as the extent of such impact and the time frame over which it may materialize. Our key non-financial indicators for 2026–2028 have been set in alignment with these hypothetical causal pathways. However, we recognize that these causal pathways are still at a stage where they will be further refined as data accumulates and analysis progresses. Going forward, we will continue to accumulate data and, through a deeper analysis of causal relationships, narrow down impactful indicators and generate new insights, thereby evolving our ability to make appropriate investment decisions in non-financial capital that lead to competitive advantage.

Enhancing corporate value

In line with the formulation of the Long-Term Vision toward 2035, we have also developed a 10-year strategy for the finance function. In this message, I have shared several of its key elements. Through the Group-wide CFO function, we will continue to advance further transformation in line with this long-term strategy, with the aim of increasing corporate value from both financial and non-financial perspectives.

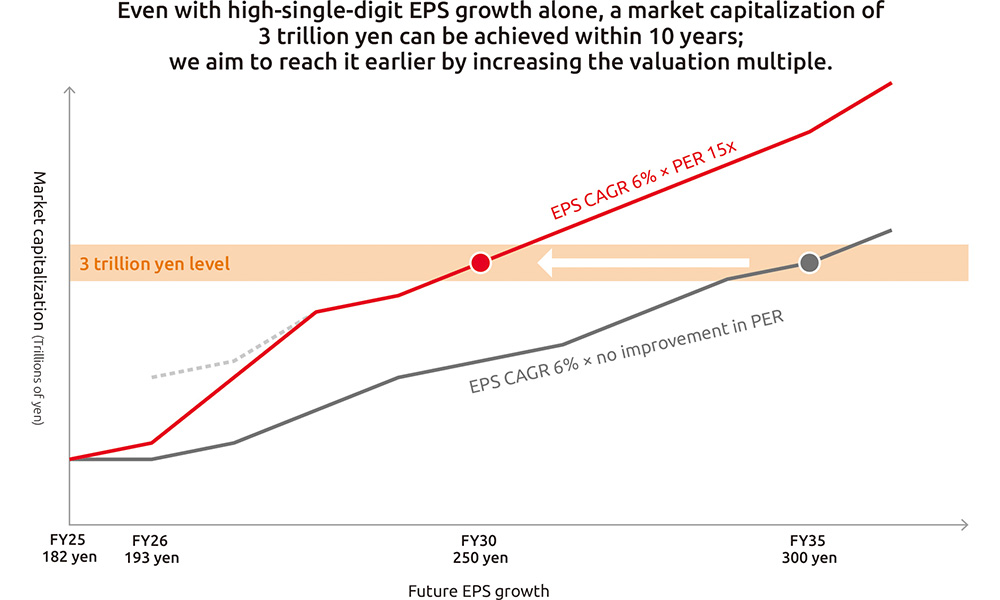

I aim to achieve the maximization of corporate value through EPS growth and an improvement in PER, and we target reaching a market capitalization of 3 trillion yen as early as possible. This level of 3 trillion yen represents a rough benchmark of approximately 1.5 times our current level. If we can sustain EPS growth at a CAGR of 6% through 2035, this target would be achievable even at the current PER. However, we aim to build investor confidence in our future growth and to reach a market capitalization of 3 trillion yen as early as possible, with the intention of expanding it further thereafter. We recognize that investors are not only focused on the growth of the Health Science Business, but are also highly interested in whether the Alcoholic Beverages Business—where volume growth is generally perceived as difficult—can continue to deliver profit growth going forward. In particular, the unification of beer taxes in Japan is scheduled for FY2026. Even amid such a significant change in the external environment, we will position this as one of our top priorities to ensure that investors continue to have expectations for sustained profit growth in the Alcoholic Beverages Business.

From FY2025, we have adopted a new dividend policy of maintaining a DOE of about 5%, together with progressive dividends. While ensuring stable and sustainable shareholder returns, we will enhance efficiency using ROIC as a key indicator and further strengthen growth investments.

We will continue to engage in constructive engagement with our shareholders and investors and fulfill our accountability, and we appreciate your continued support.